A car accident demand letter is a formal document prepared in relation to a personal injury involving a vehicle, where the injured party is requesting financial compensation. It is most commonly written by the passenger or driver who is not at fault for the accident to demand that their medical bills and other losses be covered by the at-fault party or insurance company.

The aftermath of a car accident can be overwhelming, but despite the confusion, drafting a demand letter is a crucial part of your recovery. It prepares both parties for negotiations and allows you to get the reimbursement you need to cover your damages.

What to Include in a Car Accident Demand Letter

A car accident demand Letter is a crucial part of the settlement process and may be used as evidence in court, which means it must be drafted to legal standards. It should comprise of the following key information for maximum effectiveness:

- A detailed, objective, and non-emotional account of the accident, including date and location

- An itemized list of your injury-related losses, such as medical bills and lost income

- A statement explaining why you feel the insured party should be held liable for your losses

- A detailed account of your injuries, treatment, and medication

- The amount you are requesting as compensation

- A breakdown of what the amount will cover

- A timeline within which the insurance company should process the claim

- The consequences of non-compliance

- Your or your attorney’s contact information

Tips for Writing a Demand Letter for Car Accident

Try to be as objective as possible when describing the accident and your injuries. You want to provide the reader with sufficient details of the incident from all possible aspects without losing your credibility. For example, rather than describe how scared you were during the crash, you can document the speed of the vehicles, direction of travel, and type of impact.

More tips to consider include:

- Always include supporting documents like police reports and pictures of the scene

- Calculate and include the total amount you would like to receive as compensation. if you are unsure of your losses, consult a personal injury attorney

- Send your letter via certified mail so you can confirm it was delivered to the insurance company

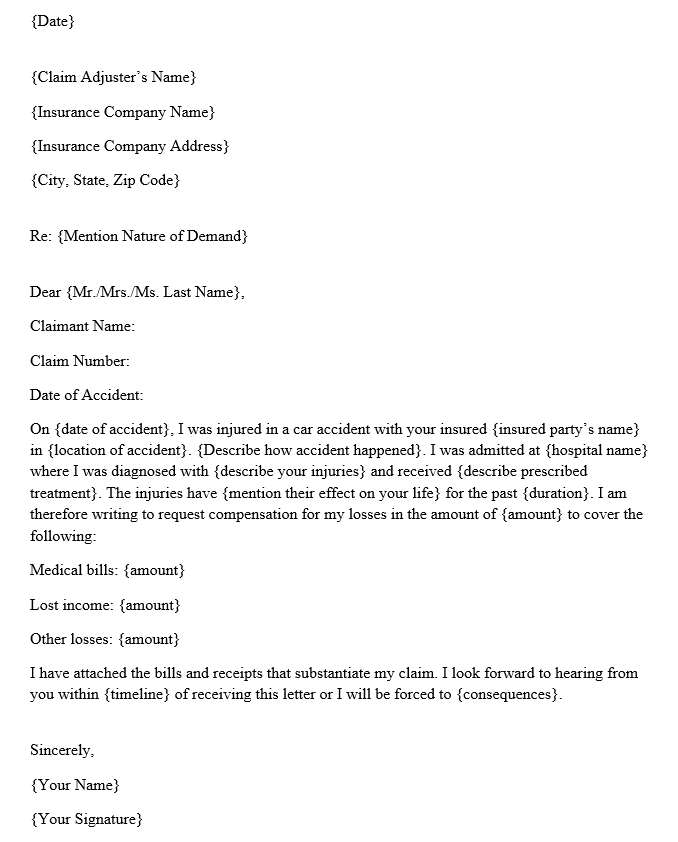

Car Accident Demand Letter Format

{Date}

{Claim Adjuster’s Name}

{Insurance Company Name}

{Insurance Company Address}

{City, State, Zip Code}

Re: {Mention Nature of Demand}

Dear {Mr./Mrs./Ms. Last Name},

Claimant Name:

Claim Number:

Date of Accident:

On {date of accident}, I was injured in a car accident with your insured {insured party’s name} in {location of accident}. {Describe how accident happened}. I was admitted at {hospital name} where I was diagnosed with {describe your injuries} and received {describe prescribed treatment}.

The injuries have {mention their effect on your life} for the past {duration}. I am therefore writing to request compensation for my losses in the amount of {amount} to cover the following:

Medical bills: {amount}

Lost income: {amount}

Other losses: {amount}

I have attached the bills and receipts that substantiate my claim. I look forward to hearing from you within {timeline} of receiving this letter or I will be forced to {consequences}.

Sincerely,

{Your Name}

{Your Signature}

Sample Car Accident Demand Letter

15 March 2031

Priscilla Fowley

Safesure Insurance Company

541 First Avenue

Dryland, MA 19900

Re: Claim No. 0008/SIC/31

Dear Mrs. Fowley,

Claimant: Lincoln Ball

Insured Party: Melisa Dennis

Claim No.: 0008/SIC/31

Date of Accident: 1 March 2031

On 1 March 2031, I was injured in a car accident with your insured Melisa Dennis in Boston, MA. I was admitted at Maryland General Hospital where I was diagnosed with severe whiplash, a broken arm, and lung puncture wounds. I have been receiving treatment there since then and I’m currently on medication for the pain.

The injuries have left me in immense pain and disrupted may aspects of my life. I have not attended work since then and the doctors project I won’t be able to for another 3 weeks. I am therefore writing to request compensation for my losses in the amount of $400,000 to cover the following:

Medical bills: $230,000

Lost income: $20,000

Other losses: $150,000

I have attached the bills and receipts that substantiate my claim. I look forward to hearing from you within 15 days of receiving this letter, or I will be forced to file a lawsuit against your insured.

Sincerely,

Lincoln Ball

Car Accident Demand Letter (Template)

Bottom Line

A car accident demand letter will usually set the stage for constructive negotiations on a suitable settlement for the injured victim. It should outline your losses as well as the compensation you would like for them. Before drafting this letter, you should always consult a personal injury attorney.