A personal injury demand letter is the first step in the negotiations regarding an injury claim. Personal injury demand letters are unique to the specific incident. Keep in mind that before you begin, minor injuries can be dealt with via the insurance company, while major injuries may require legal assistance. Also, know that these letters must be organized, portray the facts and present evidence to back up your facts.

As all personal injury demand letters are unique to the specific incident, please take this article as a basic guide to get you started. Once you’ve accomplished that, do research on how a personal injury demand letter should be written in accordance to your specific incident. Take no chances, make no assumptions, be exact and to the point.

Guide to Writing a Personal Injury Demand Letter

Your personal injury demand letter must be written in an organized manner. This means it has a beginning, middle, and an end. There is no set rule as to how long the letter should be. As long as you keep it brief and concise using easy-to-read, short sentences, you’re good. A good rule of thumb is to write the letter in an orderly manner, in such a way that anyone could follow it from beginning to end and understand the situation.

Note: Always be your own best advocate. For instance, if you slipped on Tuesday 4/10/22 around 2 pm in the afternoon, state “Tuesday, 4/10/22 at approximately 2 pm”, instead of “Tuesday, 4/10/22 at 2 pm”. If the other party has an eye-witness who states it happened at 1:45 and you write it happened AT 2 pm, the insurance company can use that against you.

Your description of damages incurred is crucial for your case. Describe the damages, including any costs and losses involved. Be specific and direct, leave no room for assumptions. Include both hard costs and intangible losses. Hard costs are those which come with evidence, such as bills for meds and clinic visits, etc.

It is crucial that your letter include all damages, both intangible losses and hard costs. Intangible losses have no hard evidence to back them up. They include such things as home much pain, suffering and emotional issues you experienced as a result of the injury. Your letter must convey to the insurance adjuster the pain and suffering you dealt with. This includes missed workdays, psychological and emotional distress, medications, and so on.

In the end, you want to provide the insurance adjuster with proof of liability. This means your case should clearly exhibit that the insured party was liable for what happened. Create a bulleted list of costs related to your injury and include it in the letter. This is your compensation amount.

Important: It is vital that you proofread your personal injury demand letter before sending. You may have your lawyer sign, seal and send the letter. If you do it on your own then use certified mail only, so you obtain a return receipt. Also, make several copies of the letter and documentation for your own records.

Basic Structure of the Personal Injury Demand Letter

Section One

This is your introduction. State who you are, along with important dates, and injuries and damages incurred. Also, the dollar amount which you are demanding and who should pay this amount.

Section Two

The middle section of the personal injury demand letter carries the weight of your negotiation. It’s crucial that you describe events leading up to your injury in a deliberate, step by step manner in chronological order. Include all details, leave nothing open to assumption.

Here you need to state the documentation you are including. With a personal injury demand letter, you must include all the documentation involved in your case. Documents include Medical records, police reports, incident reports, eye-witness testimonials, photographs and so on.

Section Three

Thank the claims adjuster for taking the time to consider your letter

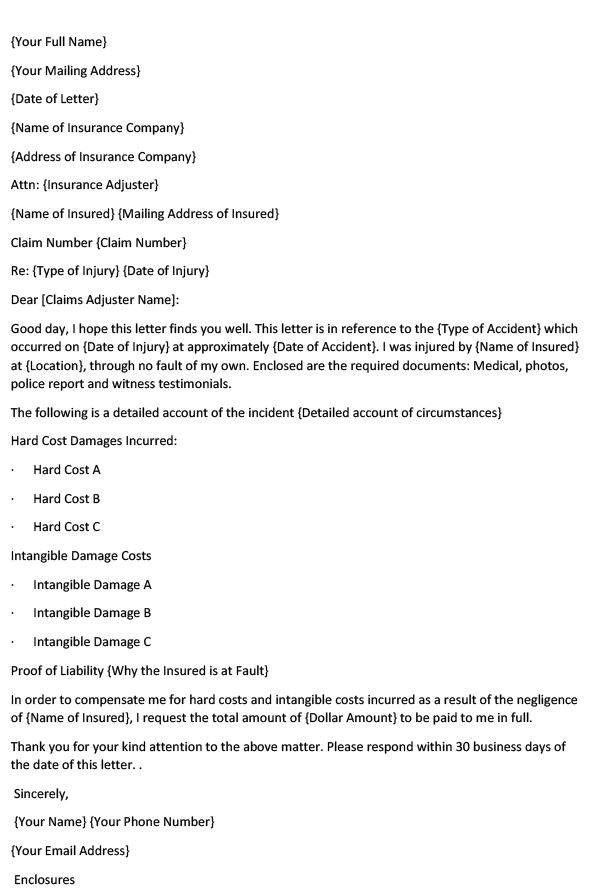

Personal Injury Demand Letter Format

{Your Full Name}

{Your Mailing Address}

{Date of Letter}

{Name of Insurance Company}

{Address of Insurance Company}

Attn: {Insurance Adjuster}

{Name of Insured} {Mailing Address of Insured}

Claim Number {Claim Number}

Re: {Type of Injury} {Date of Injury}

Dear [Claims Adjuster Name]:

Good day, I hope this letter finds you well. This letter is in reference to the {Type of Accident} which occurred on {Date of Injury} at approximately {Date of Accident}. I was injured by {Name of Insured} at {Location}, through no fault of my own. Enclosed are the required documents: Medical, photos, police report and witness testimonials.

The following is a detailed account of the incident {Detailed account of circumstances}

Hard Cost Damages Incurred:

– Hard Cost A

– Hard Cost B

– Hard Cost C

Intangible Damage Costs

– Intangible Damage A

– Intangible Damage B

– Intangible Damage C

Proof of Liability {Why the Insured is at Fault}

In order to compensate me for hard costs and intangible costs incurred as a result of the negligence of {Name of Insured}, I request the total amount of {Dollar Amount} to be paid to me in full.

Thank you for your kind attention to the above matter. Please respond within 30 business days of the date of this letter. .

Sincerely,

{Your Name} {Your Phone Number}

{Your Email Address}

Enclosures

Sample Personal Injury Demand Letter

Derek Wilson

4730 Del Rondo Drive

Tallahassee, Florida 12345

5/10/2021

ACME Insurance Company

1234 Berry Street

New York, NY 10002

Attn: Christie Parks

Your Insured: Carl Danvers

316 Turtle Drive

Monty, Florida12456

Re: Auto Collision on 4/5/21

Claim Number: 123X457z

Dear {Name of Insurance Adjuster}

I hope this letter finds you well. This letter is in regards to the car accident which occurred on 4/5/2021, at approximately 3 pm in the afternoon of that day. I, Derek Wilson, was injured when a Honda Civic, owned and driven by a Mr. Carl Danvers bumped into me while in the parking lot of Save-A-Lot foods, 5050 North Clinton Drive, Tallahassee, Florida. I was walking with my shopping cart when I was thrust forward to the pavement due to the impact of the Honda Civic bumping me from behind, through no fault of my own.

Due to the negligent action of your insured, Carl Danvers, I suffered with physical injuries, psychological and emotional pain, along with 3 weeks of work days lost. I went to my doctor, Dr. William Peterson of 3212 N. Peabody Road, Tallahassee, Florida on 4/6/2021. Dr. Peterson gave me a full examination and related the extent of my injuries, which included a fractured left femur and sprained left ankle. As a result, I lost 3 weeks of work, plus one client which could not wait for me to return.

All required documentation and photos are attached to this letter. This documentation includes a police report, medical documents, photos taken by me with my phone, and witness testimonials.

It has been approximately 30 days since the injury, and I still have not been able to recover my mobility completely. I am still under the medical care of Dr. Peterson who continues to monitor my progression. Current medical costs up to the day this letter was written, amount to $6,000.00.

Hard Cost Damages incurred due to the collision:

– Emergency room treatment…$500.00

– Medical expenses…$2,000.00

– Physical Therapy…$2,000.00

– Crutches, walker…$500.00

– Medications…$300.00

– Wages lost: $2,500.00

– Hard Cost Total: $5,300.00

Intangible Damage Costs

– Emotional distress

– Loss of consortium

– Pain and Suffering

– Intangible Cost Damages: $6,000.00

– Total Damages

As a result, I find it necessary to bring this occurrence to your attention. Hopefully, we will be able to come to a settlement. I request that I be paid the total amount of $6,000.00, as this event was due to the negligent actions of your client, with no fault of my own.

Thank you for your kind attention to the above matter. Please respond within 30 business days.

Sincerely,

Derek Wilson

derekwilson@email.com

555-555-5555

Enclosures

Personal Injury Demand Letter (Word Template)

Writing Tips

- Facts must be specific to the injury

- Include evidence, documentation, photos, witness testimonials

- Include medical bills, police reports, and other documents

- The letter should only be as long as necessary, brief and concise with short sentences

- Never exaggerate

- Send the letter via certified mail and obtain and keep the receipt for your records

Conclusion

As you can see, composing your personal injury demand letter is a complicated matter. Unless your letter is inclusive of all facts pertaining to your case, organized with the proper evidence to back up your claims, you could lose your case. Remember that each personal injury demand letter will be unique. Therefore, it is advised that you take time and study just what you’ll need for your specific case. In other words, this article serves as a basic guide only. When it comes to composing your letter, do research as to what your specific case requires. We hope we’ve helped to get you started on your journey in a positive way, so good luck and get started!